If your income is under a certain threshold, then making personal after-tax super contributions could enable you to qualify for a Government co‑contribution and take advantage of the low tax rate payable in super on investment earnings.

How does the strategy work?

If you are under 71 at the end of the financial year, earn1 less than $60,400 pa (of which at least 10% is from eligible employment or carrying on a business) and you make personal after-tax super contributions, the Government may also contribute into your super account. This additional super contribution, which is known as a co-contribution, could make a significant difference to the value of your retirement savings over time. To qualify for a co-contribution, you will need to meet a range of conditions, but as a general rule:

the maximum co-contribution of $500 is available if you contribute $1,000 and earn $45,400 or less

a reduced amount may be received if you contribute less than $1,000 and/or earn between $45,400 and $60,400, and

you will not be eligible for a co-contribution if you earn $60,400 or more.

The Australian Taxation Office (ATO) will determine whether you qualify based on the data received from your super fund and the information contained in your tax return for that financial year. As a result, there can be a time lag between when you make your personal after-tax super contribution and when the Government pays the co‑contribution. If you’re eligible for the co-contribution, you can nominate which fund you would like to receive the payment. Alternatively, if you don’t make a nomination and you have more than one account, the ATO will pay the money into one of your funds based on set criteria.

Note: Some funds or superannuation interests may not be able to receive co-contributions. This includes unfunded public sector schemes, defined benefit interests, traditional policies (such as endowment or whole of life) and insurance only superannuation interests.

Other key considerations

You can’t access super until you meet certain conditions.

You may want to consider other ways to contribute to super, such as salary sacrifice or personal deductible contributions.

Seek advice

An independent financial adviser can help you determine whether you should make personal super contributions and assess whether you will qualify for a Government co-contribution.

Includes assessable income, reportable fringe benefits and reportable employer super contributions, less business deductions and assessable First Home Super Saver amounts. Other conditions apply. ↩︎

Ryder, aged 40, is employed and earns $35,000 pa. He wants to build his retirement savings and can afford to invest $1,000 a year. After speaking to a financial adviser, he decides to use the $1,000 to make a personal after-tax super contribution. By using this strategy, he’ll qualify for a co-contribution of $500 and the investment earnings will be taxed at a maximum rate of 15%. Conversely, if he invests the money outside super each year (in a managed fund, for example), he will not qualify for a co-contribution and the earnings will be taxable at his marginal rate of 18%2.

Details

Invest outside super

Make personal super contributions

Amount invested

$1 000

$1 000

Plus co-contribution

Nil

$500

Total investment

$1 000

$1 500

Tax rate payable on investment earnings

18%

$15%

If you have questions or need guidance, talk to your independent financial adviser or get in touch with us on 1300 451 339. We can help you understand what the changes mean for you and how to make the most of your support.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 16 December 2025.

Big changes are coming to home care from 1 November 2025 when the new Aged Care Act begins.

If you are currently receiving help through a Home Care Package, it’s important to understand what will change for you, including how your care services are managed and what you might need to contribute from 1 November.

Talk to your care provider, and if you’d like some advice, we’re here to help.

What’s changing

On 1 November, everyone receiving a Home Care Package will transfer to the new Support at Home program. What this means for you will depend on your situation and the choices you make, but two key changes you will notice are how the fees work and what happens if you don’t spend your full budget allowance.

New fee structure

The Government will continue to pay a large portion of the cost for your home support but you will be asked to contribute a share of the cost. To determine your contribution, services will be grouped into three categories:

Clinical care

Independence support, and

Everyday living.

The government will fully fund clinical care services, but you will be asked to make a contribution towards the cost of other services. How much you contribute depends on your financial situation – with age pensioners paying less than self-funded retirees.

The new fees are likely to be higher, but if you were receiving a Home Care Package (or held approval for one) on 12 September 2024, you’ll be eligible for grandfathering concessions (and lower rates) to ensure you are “no worse off” under the new rules.

Unspent funds

Another big change is how your spending budget works.

Each quarter you’ll be given an available budget based on your package level. This is made available on a “use it or lose it” basis. If you don’t use all the money in that quarter, you can only carry over up to $1,000 or 10% of your quarterly budget (whichever is greater). The rest of the money is no longer available.

Unspent funds that you have accumulated at 31 October 2025 may remain available to spend on approved services at a future date.

What you should do now

To help you get ready for the changes, all Home Care Package recipients should have received a letter from the Department of Health, Disability and Ageing, explaining whether you are grandfathered and what contribution percentage rates you can expect to pay.

Keep this letter safe – and share a copy with your independent financial adviser. They can help you to understand what it means for your finances and make sure you are set up to manage your costs.

Your contribution rates will be confirmed in a second letter from Services Australia after 1 November. Before 1 November, you should also speak to your care provider to review your care plan and sign a new care agreement based on their new pricing structure.

If you have questions or need guidance, talk to your adviser or get in touch with us on 1300 451 339. We can help you understand what the changes mean for you and how to make the most of your support.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 29 October 2025.

From 1 November 2025, a new program called Support at Home will replace the current Home Care Package system, bringing significant changes.

On the positive side, there will be more packages available, which should reduce waiting times. But there will also be changes to the contributions (fees) you pay – and for some people, this could mean paying more for the care services you access.

Here’s a simple overview to help you understand what’s changing and how you can prepare.

What’s changing?

The existing Home Care Packages will cease on 1 November 2025, and everyone will transition to Support at Home. You might not see a disruption in your services, but you will notice changes.

Some key differences in the new system:

A new fee structure, based on your financial circumstances and the services you access

You will continue to be charged by your provider, but only after you have received services

Eight levels of care instead of four, to better match your needs, with additional funding for assistive technology and home modifications (where approved)

Budgets will be allocated quarterly – and if not used, won’t carry over.

These changes apply to both new applicants and people who are already receiving care.

What about fees?

The Government will continue to subsidise care costs within your approved budget, but you’ll be expected to make a contribution. Here’s how the new contributions will work:

What you pay depends on your financial situation – whether you receive a full or part pension, or are self-funded

Clinical care (like nursing or physiotherapy) will be fully funded by the Government

You may pay more for everyday living services (like meal preparation or cleaning) than you do for independence supports (like personal care or transport).

If you were approved for, or receiving, a Home Care Package as at 12 September 2024, you will be eligible for fee concessions, so you are no worse off under the new rules.

Importantly, there’s a lifetime cap on your contributions – you will not pay more than $130,000 (indexed) over your lifetime.

Your package level sets the total funding available to pay for care, but 10% is allocated to the care provider to cover the cost of care management. You then work with your provider to decide how you want to spend the rest of the budget. The provider sets their fee for services so it’s worth checking what they charge – the more they charge, the less support you may be able to afford from your package. You could always choose to pay extra if your package does not cover all the care you need.

How to be ready?

To make the most of the new system, it’s a good idea to take a few steps before November:

Think about your care needs – what help do you need and what services will make a difference to you?

Talk to your current provider – if you’re already receiving care, they should be in touch to help you transition. You’ll need to sign a new service agreement under the new system.

Book an assessment – if you need help but don’t already have a package, contact My Aged Care to arrange a care needs assessment. This takes time, so it’s best not to delay.

Need help to understand your options?

Navigating aged care can be complicated – especially with these new changes. That’s why we offer specialist aged care advice to help you plan and make the best choices.

We can help you:

Understand how the changes affect you

Calculate estimates of your contributions

Make sure your finances and investments are set up to provide the cashflow you’ll need.

If you’d like to chat about your options or get help preparing for the changes, we’re here to help. Just give us a call.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 20 October 2025.

If you or a loved one is moving into aged care, you’ve probably noticed that room prices are going up. In fact, they’ve already increased significantly in 2025 – and more changes are on the way.

Prices are rising

Since the start of 2025, the average cost of a room in aged care has gone up by about $46,000. This brings the average refundable accommodation deposit (RAD) to $572,589 as of July 2025 – up from $526,859 in December 2024. That’s an increase of 8.7%.

If you choose not to pay the lump sum RAD and instead pay the daily accommodation payment (DAP), this could make the ongoing fees higher too (depending on interest rates) – potentially adding thousands of dollars each year in daily “rent”.

Why the increase?

There are a couple of key reasons for these rising prices:

The RAD approval threshold has increased – on 1 January 2025, the government raised the RAD threshold from $550,000 to $750,000 (now indexed to $758,627). RADs can be higher than $750,000, but providers need approval before they can charge higher amounts.

Providers are under pressure – rising operating costs have pushed many aged care providers to increase their prices.

Since January, around 1,200 residential aged care homes have increased room prices – and not just the most expensive ones. Even lower-cost rooms have seen price hikes. That said, not all providers raised their prices. Interestingly, more than 80 providers have reduced the highest price in their facilities.

What’s next?

Higher room prices mean you may need to use more of their savings or income to cover aged care costs.

And from 1 November 2025, a big change is coming. Anyone who moves into care after this date and pays a RAD, will have 2% of that amount deducted each year, for up to 5 years. That means you could lose up to 10% of your RAD over time. This amount won’t be refunded to your estate.

If instead you choose to pay the DAP, the cost will go up every six months (March and September) in line with inflation.

How does it work?

Let’s look at three sample situations:

Adam moved into care in December 2024 and agreed to pay a room price of $526,000. He will get back the full amount of any RAD paid when he leaves care (minus any fees he has asked to be deducted along the way).

Annabelle moved into care in July 2025 and agreed to a room price of $572,000. Her RAD is fully refundable as well, but if she chose to pay the DAP, this would be a bit cheaper than Adam’s because interest rates have dropped over the year. But if the interest rates had gone up (or stayed the same), her daily fee would be higher.

Arturo moves in after 1 November 2025. He also agrees to a room price of $572,000. But under the new rules, he will lose 2% per year from any RAD paid (up to 10% in total over five years). If he chooses to pay the DAP instead, the amount payable will increase every six months with inflation.

What should you do?

The rules are set by the government, so you can’t avoid paying for your room in care. However, some people with lower financial means may qualify for a subsidised room.

What’s most important is to understand your options and costs, and how they affect your financial future. Everyone’s situation is different, so getting advice from a licensed independent financial planner can really help – especially with decisions about how to pay, how much to pay, and how this affects your estate and long-term finances.

If you need to move into care now, doing it before 1 November 2025 might help you avoid the new RAD deductions and save money in the long run. But rooms are hard to find and competition is high.

If you want to find out more for your situation, call us on 1300 451 339 to arrange an appointment.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 13 October 2025.

After a five-year freeze, deeming rates are set to increase on 20 September 2025. For some older Australians, this may not be a welcome change.

An increase in deeming rates increases assessable income for Centrelink and Veterans’ Affairs, which may reduce entitlements and/or increase aged care fees. But for many people, the impact may not be significant.

Why the change?

Deeming is used to determine a level of assessable income from your financial investments – bank accounts, shares, managed funds, some superannuation and income streams, loans you have made and excess gifting.

Deeming rates are usually reviewed twice a year, in March and September, to reflect changes in market rates, but have been frozen for the last five years, originally to support pensioners through the uncertainty of COVID.

From 20 September 2025, the deeming rates will increase to:

0.75% on financial assets up to the lower threshold (currently 0.25%)

2.75% on financial assets above the upper threshold (currently 2.25%)

Today, the cash rate sits around 3.6%. Against that backdrop, a 0.5% rise in deeming is relatively modest.

Who will it impact?

For most retirees, the assets test has a greater effect on Centrelink entitlements than the income test, so the deeming rate increase may have little impact. However, you will feel the change if:

Your Centrelink/DVApayments are determined by the income test.

You are an aged care resident, as higher deemed income might result in higher ongoing care fees.

You are a part-pensioner, or a self-funded retiree with a Commonwealth Seniors Health Card, and you pay an income-tested fee for your current Home CarePackage or will start to receive Support at Home packages from 1 November 2025.

In these circumstances, higher assessable income may have a detrimental effect on your entitlements or fees. Individual calculations are needed to determine what impact this might have on you.

A potential silver lining

Interestingly, there is a benefit for aged care residents who leave residential care.

When you leave, aged care providers must refund the balance of your Refundable Accommodation Deposit (RAD) and also pay interest (from date of departure until date of payment). This interest is based on the lower deeming rate applicable the day after care ends. The higher deeming rate will provide a financial boost to the estates of those exiting care after 20 September 2025.

What should you do?

If you’re currently receiving Centrelink or DVA benefits, or contributing to aged care costs, it’s worth reviewing your situation ahead of the September change. In many cases, the effect will be minimal, but for some, even small shifts in assessable income can influence entitlements or fees and put pressure on your cashflow.

If you need help to ensure you’re making the most of your retirement income and benefits call our office today on 1300 451 339 to discuss your situation.

IMPORTANT INFORMATION: This information has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 6 October 2025.

Generally, your total super balance (TSB) is the sum of all amounts you have in the superannuation system (certain exceptions apply*). At a high level, it includes:

your accumulation account balances

your superannuation pension accounts, and

the outstanding balance of a Limited Recourse Borrowing Arrangement (if you have a self-managed super fund which has borrowed to invest), in certain circumstances.

TSB is used as part of the eligibility criteria for certain types of super contributions.

* Exceptions and modifications may apply, for example if you’ve made a personal injury contribution to super. Calculating TSB can be complex, so it is important to seek advice.

When is it measured?

Your TSB for a financial year is measured on the previous 30 June when determining your eligibility

to make or receive certain types of super contributions.

How does TSB impact contributions?

Eligibility rules apply to the different types of contributions that can be made to super. Some contributions require that your TSB is below certain thresholds (usually generally based on your TSB at the previous 30 June). For this reason, it is important that you carefully check your TSB before making contributions to super. Also, your financial adviser might need to know details of your TSB to ensure that any recommendations to contribute to super are within your contribution caps^.

^ The contribution caps limit the amount that can be contributed to super. The amount you can individually contribute (or have made on your behalf) depends on a number of issues including your TSB. Exceeding your contribution cap may result in additional tax or penalties. Visit ato.gov.au for more information.

How to check your TSB

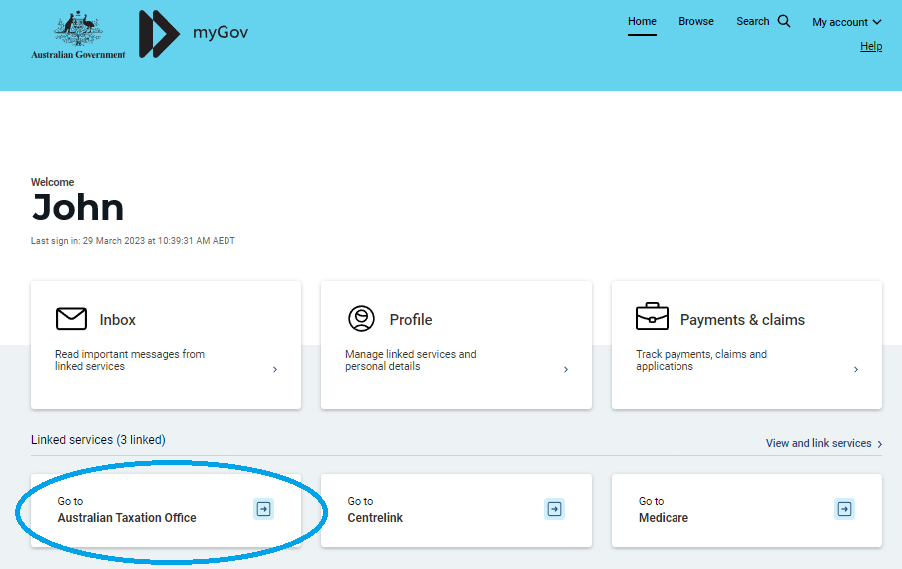

There are a few ways you can track your TSB. A useful source of information is your MyGov account which

is explained below. Other options are contacting your superannuation funds or looking at your fund’s statements and records. When reviewing your annual statement, the TSB figure your fund reports to the ATO is usually referred to as ‘exit value’ or ‘withdrawal benefit’. This may be different to the 30 June ‘closing balance’.

How to track your total super balance

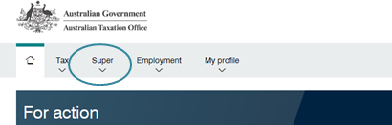

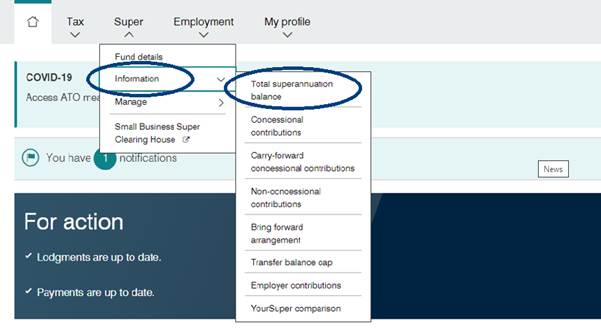

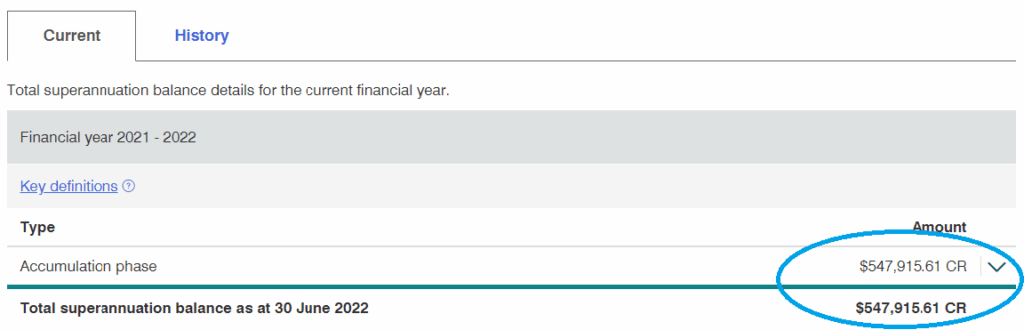

Login to you MyGov Account by visiting my.gov.au *

Click the Information option and then the Total superannuation balance.

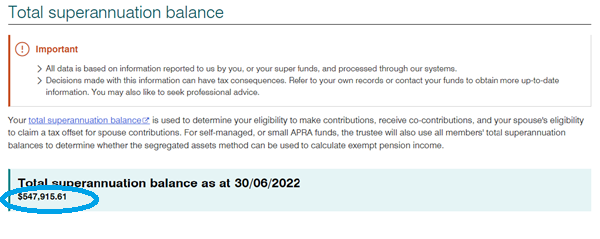

The most up to date TSB recorded by the ATO for the prior 30 June is displayed.

Note the TSB displayed at a time may not accurately reflect all of your super interest as t 30 June. This is because of the timing of super fund reporting requirements to the ATO, which may not be completed until October (or later for some SMSFs).

Click on the drop-down arrow to the right of each super interest to reveal detailed account information.

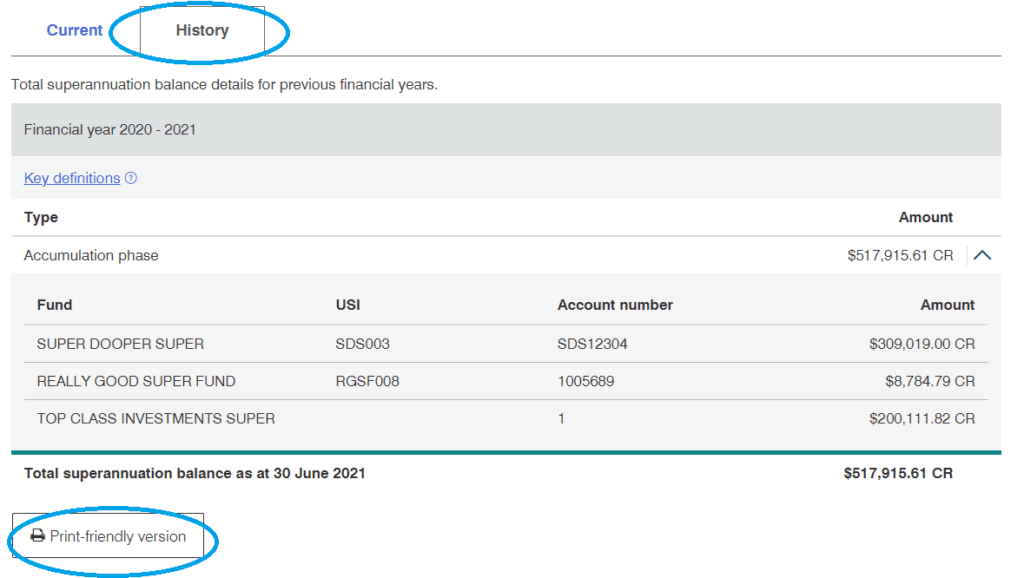

Click History button to display prior year’s 30 June TSB.

Click Printer friendly version button to open the data in a format appropriate to print.

Check the information provided.

Remember that your TSB reflects your accounts as at the prior 30 June. Before you rely on the information in MyGov, it is important that you:

Check that all of the super and pension accounts that you held on 30 June are displayed

Reconcile the amounts displayed with the ‘exit’ or ‘withdrawal’ value displayed on your end of year statements and other records, and

Contact your super fund and the ATO if the information doesn’t look correct before making super contributions.

For more information speak with your independent financial advisor or visit the ato.gov.au

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 29 September 2025.

Big changes are on the way for aged care, with new rules starting from 1 July 2025. While these changes aim to create a more sustainable and fairer system, they do bring added complexity — especially when it comes to understanding the fees and making the right financial decisions.

Here are the five key things you need to know:

1. Aged care will cost more – but is still subsidised If you or a loved one is moving into residential aged care after 1 July 2025, the amount you’ll need to contribute will be higher. That said, the Government will continue to fund a large share of care costs – around 73% on average. But it will be important to consider your cashflow.

2. Expect new terminology and fee calculations The language is changing. Instead of the current “means-tested care fee,” you’ll now see new names like Hotelling Contribution and Non-Clinical Care Contribution. How much you are asked to pay will still be based on your income and assets, but new formulae may result in higher contributions than under the current rules.

3. Lifetime caps remain – but at a higher level A lifetime cap will continue to apply to limit how much you can be asked to pay as a non-clinical care contribution over your total stay in residential care. This cap is increasing to $130,000, but with a new safeguard, that no matter how much you pay, you will only need to pay this fee for a maximum of four years. This helps ensure fairness between residents with different levels of wealth.

4. Retention amounts are being reintroduced If you choose to pay a lump sum for your room (known as a refundable accommodation deposit – RAD), aged care providers will deduct a “retention amount” of up to 2% per year (capped at 10% over five years). While this increases the cost slightly, it may still be better value than paying the daily accommodation payment.

5. Good advice can prevent costly mistakes Navigating these new rules can be confusing – especially when you need to make major decisions about the family home, assets or pension entitlements. The cost of getting good advice is often small compared to the cost of getting it wrong. That’s why seeking qualified aged care independent financial advice is more important than ever.

If you’re starting to think about aged care for yourself or a family member, now is the time to start planning and seek advice. As specialists in aged care advice, we can help you to make informed decisions with confidence and peace of mind. Call us today on 1300 451 339. IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 15 April 2025.

After a long wait, new legislation which is aimed at reshaping how aged care is delivered and funded in Australia has been passed.

Like most countries around the world, our population continues to age, making it important to have a sustainable aged care system that provides quality care and treats our older Australians with dignity. But this also requires adequate funding.

The new Act is founded on person-centred principles that puts you as the user of care services, in the centre. The aim is to provide more choice and greater control, as well as defined rights for older Australians.

But the money is what most people are worried about. So, here’s what you need to know to stay informed and make sure you can afford the care that you need and want.

Who is affected?

The rights in the Aged Care Act apply to everyone, but the new rules for fees will only apply if you move into residential care after 30 June 2025 or are approved for Home Care after 12 September 2024.

If you were receiving a Home Care Package as at 12 September 2024 (or had been approved and in the queue waiting for a package to be allocated), grandfathering rules apply. The aim is to ensure you are not disadvantaged by some of the rule changes even if you move into residential care after 30 June 2025.

What is changing for residential care?

Some room prices may increase but we still expect to see a range of price points. And you will still be able to choose to pay for your room as a lump sum or as daily “rent”.

If you pay a lump sum, each year the provider must deduct and keep 2%. This only applies for the first five years so you could lose up to 10% of the amount paid, with the remainder refundable to you or your estate. If paying the daily accommodation payment (“rent”), this increases each six months in line with inflation.

Ongoing care costs will be split between you and the government, with three new fee categories to work out this split:

Everyday living expenses – currently $63.57 (indexed) per day, but if you have assets over $238,000 or income above $95,400 (or a combination) you may pay up to an additional $12.55 per day.

Non-clinical care – this is a means-tested fee of up to $101.16 per day. It will only apply for the first four years, or up to a dollar cap of $130,000 (indexed).

Clinical care – this is the most expensive component and will be fully paid for by the Government.

What is changing for home care?

The Support at Home program starts on 1 July 2025, expanding care to eight levels instead of just four. Similar to residential care, the costs will be split into three categories and means-tested to work out how much you pay:

Clinical care will be fully paid by the government.

Self-funded retirees will pay 50% of the costs for independence support and 80% of everyday living costs.

Full pensioners will pay only 5% of independence support costs and 17.5% of everyday living costs.

The percentage part-pensioners and holders of a Commonwealth Seniors Health Card will pay is between the above two groups and is based on means-testing.

Your home care contributions are subject to a $130,000 (indexed) lifetime cap.

An important change is to note that the package budget will be allocated quarterly, on a ‘use it or lose it’ basis. You will only be able to roll over unused funds up to $1,000 or 10% of the package budget from quarter to quarter.

What do you need to do?

Navigating these changes can be complex so ensuring you have kept enough money to meet your care needs in the later years of life is vital to maximise your quality of life.

If you or a loved one require aged care, acting before 1 July 2025 may help you lock in current fee arrangements. But whenever you decide care is needed, it is important to get comprehensive independent financial advice to fully understand your options and how to restructure your assets and investments.

As a licensed independent financial adviser and Accredited Aged Care Professional™ we have the experience and expertise to help. If you wish to discuss your situation, call our office on 1300 451 339 to make an appointment with us.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 18 March 2025.

By making a personal super contribution and claiming the amount as a tax deduction, you may be able to pay less tax and invest more in super.

How does the strategy work?

If you make a personal super contribution, you may be able to claim the contribution as a tax deduction and reduce your taxable income. The contribution will generally be taxed in the fund at the concessional rate of up to 15%1, instead of your marginal tax rate which could be up to 47%2. Depending on your circumstances, this strategy could result in a tax saving of up to 32% and enable you to increase your super3.

How do you claim the deduction?

To be eligible to claim the super contribution as a tax deduction, you need to submit a valid ‘Notice of Intent’ form to your super fund within required time frames. You will also need to receive an acknowledgement from the super fund before you complete your tax return, start a pension, withdraw or rollover money from the fund or scheme to which you made your personal contribution.

Make sure you can utilise the deduction

It is generally not tax-effective to claim a tax deduction for an amount that reduces your assessable income below your tax free threshold. This is because you would end up paying more tax on the super contribution than you would save from claiming the deduction.

Other key considerations

Personal deductible contributions count towards your ‘concessional contribution’ cap. This cap is $30,000 in FY 2024/25, or may be higher if you didn’t contribute your full concessional contribution cap in any of the previous five financial years and are eligible to make ‘catch-up’ contributions. Tax implications and penalties may apply if you exceed your cap.

You can’t access super until you meet certain conditions.

If you are an employee, another way you may be able to grow your super tax effectively is to make salary sacrifice contributions (see below)

Seek advice

To find out whether you could benefit from this strategy, you should speak to an independent financial adviser and a registered tax agent.

Case study

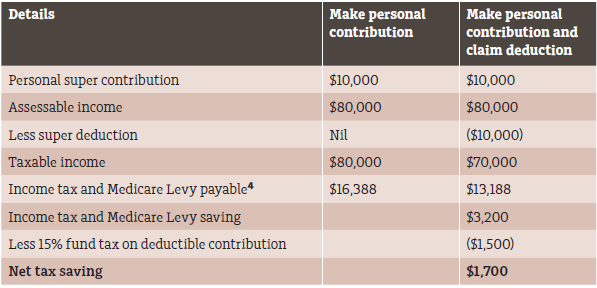

Bill, aged 55, is self-employed, earns $80,000 pa and pays tax at a marginal rate of 32% (including the Medicare levy). He plans to retire in 10 years and wants to boost his retirement savings. After speaking to an independent financial adviser, he decides to make a personal super contribution of $10,000 and claim the amount as a tax deduction. By using this strategy, he’ll increase his super balance. Also, by claiming the contribution as a tax deduction, the net tax saving will be $1,700. If the tax deduction is claimed on the personal contribution, $8,500 (his contribution net of tax withheld) is invested in super. If no deduction is claimed, $10,000 is invested in super. However, no tax savings are applied to Bill’s income tax assessment for the relevant year.

Salary sacrifice contributions

If you are an employee, you may want to arrange with your employer to contribute some of your pre-tax salary into super. This is known as ‘salary sacrifice’.

Like making personal deductible contributions, salary sacrifice may enable you to boost your super tax-effectively. There are, however, a range of issues you should consider before deciding to use this strategy.

We can help you determine whether you should consider salary sacrifice instead of (or in addition to) making personal deductible contributions.

Individuals with income above $250,000 in FY 2024/25 will pay an additional 15% tax on personal deductible and other concessional super contributions. ↩︎

IMPORTANT INFORMATION: This information has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 6 March 2025.

Did you know that you may be able to make voluntary contributions to super to help save for a deposit on your first home? What are the potential benefits of using super? We explain more about the scheme below.

Tell me the basics – how does it work?

When it comes to saving for your first home, super probably isn’t an investment option that springs to mind. Generally, super can only be accessed once you’ve retired or met another ‘condition of release’, which could be a long way down the track.

However, under the First Home Super Saver Scheme, you may be able to make voluntary contributions to super, and you may be eligible to withdraw these amounts, plus associated earnings to put towards a deposit on your first home. Below, we highlight the key steps you need to follow.

Why use super to save?

There are a few potential benefits to using super to save for a home deposit, including:

earnings in super are taxed at up to 15% and are concessionally taxed when you make a withdrawal from super under the scheme. Earnings on investments or bank accounts in your own name are taxed at your marginal tax rate (MTR) which could be up to 47%[1], and

depending on the type of contributions you make, these amounts may reduce your taxable income for the year and therefore reduce tax payable.

The tax effectiveness of the scheme may free up more of your hard-earned funds and increase the amount you can save for that home deposit.

Am I eligible?

To be eligible for the FHSSS, you must meet certain conditions, including:

be aged 18 years or older at the time you apply to withdraw the funds

have not ever owned or had an interest in Australian real estate (including residential, investment and business properties) unless you meet financial hardship provisions, and

make voluntary super contributions.

What contributions can I make and access under the FHSSS?

You can make voluntary contributions of up to $15,000 per year within your ordinary contribution caps and can withdraw a maximum of $50,000 of voluntary contributions plus earnings on the amount you withdraw. You can read more about the different types of contributions and contribution caps at ato.gov.au.

Voluntary contributions include:

Voluntary contributions do not include:

Applying to have funds released

There are some important steps and timeframes you must understand.

1. Request and receive a FHSS determination

A FHSS determination provides you with the maximum amount you’re eligible to withdraw. You can request a determination via myGov. You’ll need to have requested and received a determination from the Australian Taxation Office (ATO) before signing a contract of sale or for construction[2], or purchasing a home at auction. If you don’t, you won’t be eligible to access the contributions you’ve made to super.

2. Request to withdraw funds

Provided you’ve received your FHSS determination, you may request to release (or withdraw) an amount up to the figure noted in the FHSS determination before or after you sign a contract. However, if you apply for the release authority after you’ve signed a contract, you need to make the request within 90 days of entering a contract. A release request can be made via myGov.

After the funds are released, there are additional requirements and obligations – see below.

Taxation of funds

Some of the amount withdrawn is subject to tax (known as the assessable amount). This includes any concessional contributions[3] that are released to you, plus any associated earnings that have accrued on any of the contributions released to you (either concessional or non-concessional). The assessable amounts are taxed at your MTR less a 30% tax offset. The ATO will estimate your income for the year in which you withdraw the funds and will withhold tax from the amount paid to you at your estimated tax rate[4].

What happens after applying to release funds?

It generally takes the ATO between 15 and 20 business days after your release request to send the funds to you (see ato.gov.au). You’ll need to purchase a home or sign a construction contract within 12 months of receiving the funds. If you don’t, the ATO automatically provides an additional 12 month extension to you, and will notify you in writing. After you sign a contract, you must notify the ATO within:

28 days, if using a FHSS determination dated on or before 14 September 2024, or

within 90 days if using a FHSS determination dated on or before 14 September 2024.

You must move into your home as soon as possible after purchase or construction is complete, and you must intend to live there for at least six of the first 12 months.

If you still haven’t purchased a home or signed a construction contract within that timeframe, you’ll need to either:

recontribute the funds to super as a non-concessional contribution[5] for which you can’t claim a tax deduction and notify the ATO via myGov, or

pay FHSS tax of 20% on the assessable amount that was released to you, which is in addition to any tax payable on the withdrawal[6].

What if you change your mind?

If you change your mind after you’ve contributed to super and no longer intend to purchase a home, the money you’ve contributed to super won’t be accessible.

If you change your mind after the funds have been released, you’ll need to either recontribute the money to super, or pay additional FHSS tax. If you change your mind before the funds have been released, you can amend or withdraw your FHSSS application. You can then re-apply in future should the need arise once you have withdrawn your application.

What next?

To find out more about the FHSSS and to understand the different ways you can contribute, and the benefits it may provide to you, we recommend you seek financial advice and visit ato.gov.au. You may also be eligible for state/territory based stamp duty concessions or first home buyer grants and you should seek further information from the revenue office in your location.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 10 February 2025.

[2] If you’re building a home, you need to ensure you have applied for a FHSS determination before purchasing vacant land

[3] Concessional contributions include personal contributions which you have claimed as a tax deduction and salary sacrifice amounts

[4] If the ATO can’t estimate your income for the year and therefore your MTR, they will withhold tax on the assessable amount at 17% and any adjustment will occur when you submit your tax return for the year.

[5]The contribution counts towards your non-concessional contribution cap. Tax penalties may apply if you exceed your cap.

[6] This will also apply if you recontribute the amount to super but you don’t notify the ATO

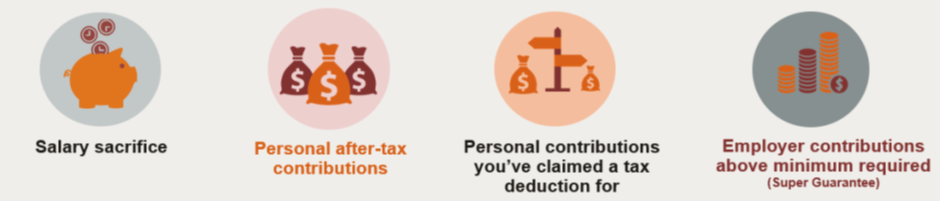

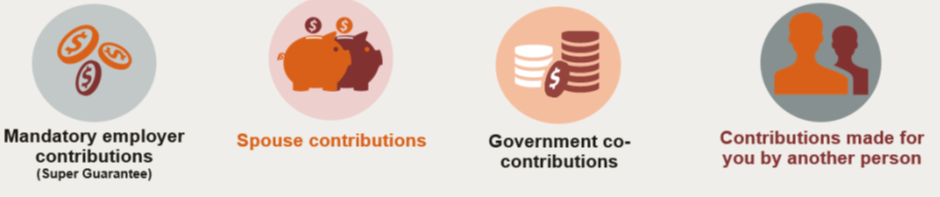

Non-concessional contributions (NCCs) include personal contributions made to super from after-tax income or other available savings. Limits apply to the total NCCs that you can contribute to super without exceeding your contribution limit. To help avoid breaching the cap, you can access your contribution information on myGov.

What are non-concessional contributions?

Non-concessional contributions (NCCs) include those made with after-tax money, such as your take home pay, or funds in your bank account. NCCs may provide significant opportunities to build super for retirement. NCCs form part of the tax-free component of your super interest and are not taxed when released from super.

NCCs commonly include:

personal contributions for which a tax deduction is not claimed

spouse contributions

excess concessional contributions not released from super, and

certain amounts transferred from a foreign super fund.

Am I eligible to make NCCs?

To be able to make NCCs, you need to meet certain eligibility rules. This includes:

you’re aged under 75 at the time you make the contribution[1], and

your ‘total super balance’[2] at the previous 30 June is less than certain limits (see below).

Limits on NCCs

Like other contribution types, there are limits on the total amount of NCCs you can contribute to super and penalties apply if limits are breached. For more information on excess contributions, see ato.gov.au.

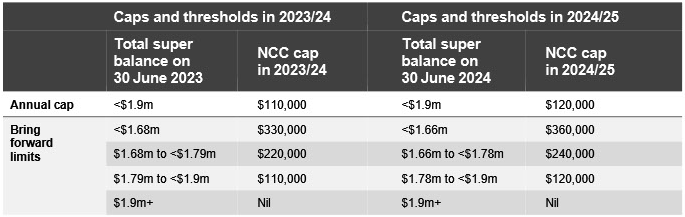

In 2024/25 the annual NCC cap is $120,000. However, depending on your total super balance, you may be able to use the bring forward rule to make even larger contributions sooner. This rule may enable you to bring forward up to two years’ worth of NCCs in addition to the current year’s cap.

What’s my limit?

Your eligibility to contribute up to the annual NCC cap – or larger amounts under the bring forward rule – is determined based on your total super balance. The limits for the current and next financial years are summarised in the table on the following page. You can check your total super balance details using myGov.

A subsequent post deals with howto access your total super balance details.

How to access non-concessional contribution details on myGov

There are a few ways you can monitor your NCCs and to check whether you’re currently in a bring forward period.

The steps to using myGov to access NCC information are explained below. However, it is recommended that detailed records also be maintained and referred to. This is because there may be a delay before your super fund reports details about your contributions to the ATO. Remember, additional tax applies for excess contributions.

Note: The below screenshots and scenarios relate to different fictional individuals and are used to show you the possible NCC and bring forward data on myGov.

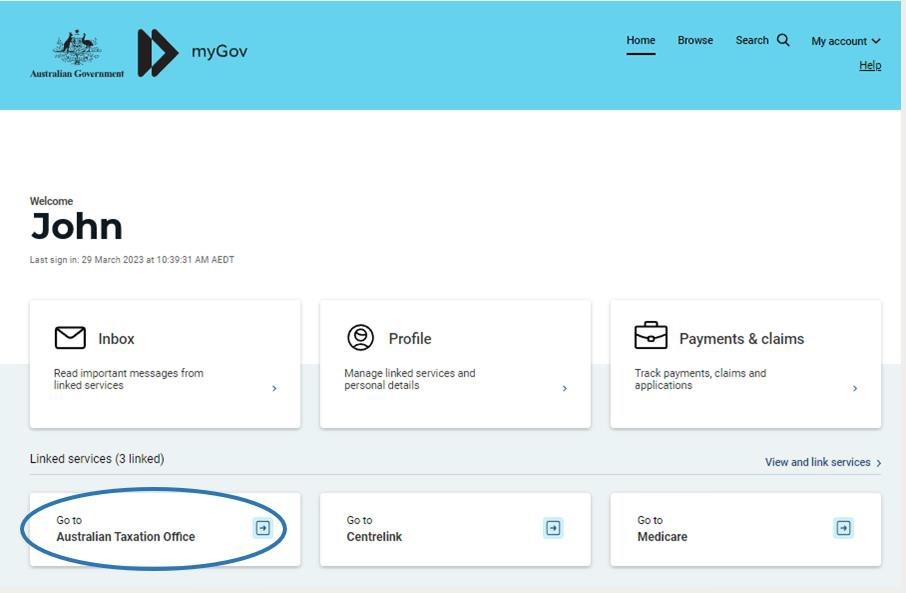

Step 1: Login to your myGov account by visiting my.gov.au and select the ATO service

Haven’t linked your myGov account to the ATO? Use the link below and follow the steps. Click here for instructions onhow to link the ATO to myGov or visit: https://my.gov.au/en/about/help/mygov-website/link-services-to-your- account/link-the-australian-taxation-office

Step 2: Select the ATO service

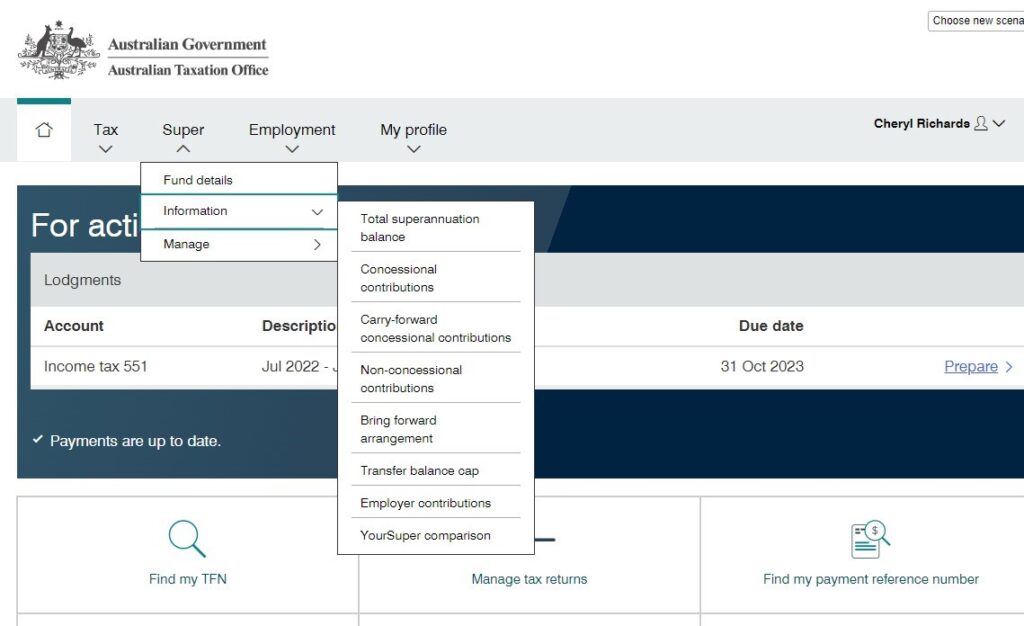

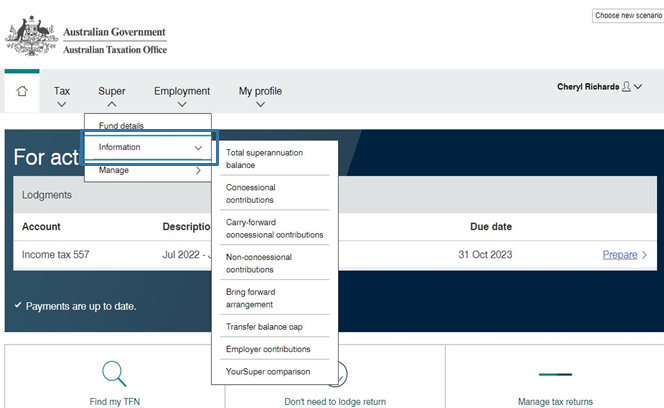

Step 3: Select the ‘Super’ tab

Step 4: For information on NCCs, click on the ‘Information’ option and a second menu will be revealed. Click ‘Non- concessional contributions’.

Step 5: For information on NCCs, click on the ‘Information’ option and a second menu will be revealed. Click ‘Non- concessional contributions’.

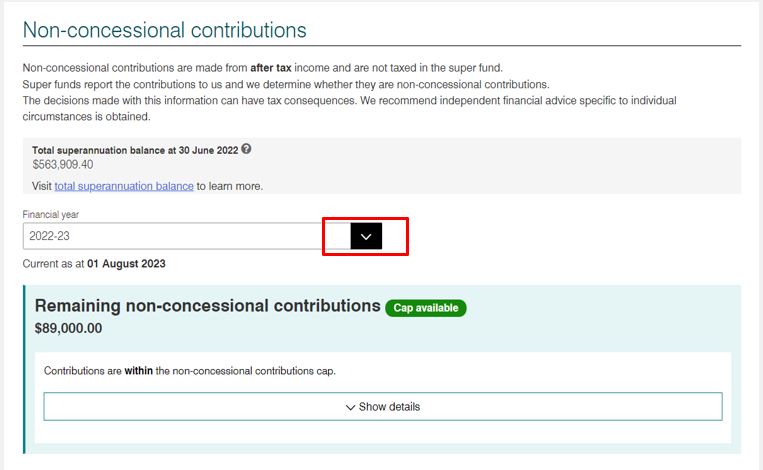

Use the arrow (red box) to reveal a drop-down list to select a financial year. Information regarding the NCCs made during that period will be displayed.

Your TSB as at the 30 June prior to the relevant financial year is displayed, provided ATO have this information. See note below

Click on ‘show/hide details’ (black box) to reveal the NCCs reported to the ATO for the period selected. In this example, the person has $89,000 of their NCC cap remaining

Note: The information shown reflects the information that the ATO has received from your super funds to that point. If there is a delay in any of your funds reporting to the ATO, or there has been an error in reporting, the information displayed will not be accurate. Funds do not report your 30 June total super balance often until some months into the new financial year. It is important to maintain your own records and ascertain contribution information from other sources, such as your super fund or financial adviser, to determine contribution eligibility.

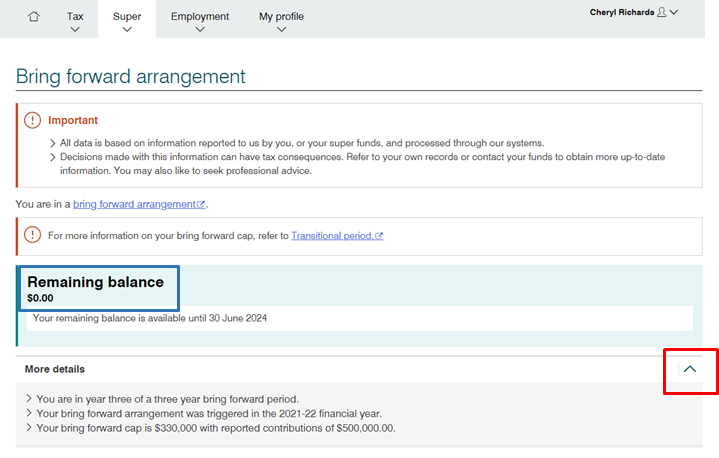

Step 6: For information on bring forward arrangements, click the ‘Super’ tab, and then ‘Information’ to reveal a second menu. Select ‘Bring forward arrangement’

Step 7:This screen will display information regarding any bring forward arrangement that you may be in. This means you may have previously triggered the bring forward rule within the last three years.

Your available NCCs will be displayed in the ‘remaining balance’ box (blue box). For an explanation of the amount displayed, click on the drop down arrow (red box). As seen in this example, the individual is currently in a three year bring forward period, after triggering the arrangement in 2021/22. They have fully utilised their available limit.

Next steps

Contribution rules and eligibility criteria for NCCs and the bring forward provisions are complex. This guide is not designed to provide comprehensive information about how the rules work or how they may apply to you. It is recommended that you speak with an independent financial adviser and visit ato.gov.au for more information.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 10 January 2025.

[1] Contributions must be received by your fund no later than 28 days after the month you turn 75

[2] Total super balance includes the total of all amounts you hold in super accumulation and pension accounts, in-transit rollovers, and if you have a self-managed super fund, it may also include the outstanding balance of a limited recourse borrowing arrangement. The total Is reduced by personal injury or structured settlement contributions made to super.

Cashflow planning is important when moving into aged care, but plans can be thrown into chaos if your first invoice shows much higher fees than expected. This article sheds light on interim fees.

The first statement you receive when you move into residential aged care can be a shock, as fees might be far higher than expected – possibly even hundreds of dollars a day higher. This might not be an error but rather be just a matter of understanding how “interim fees” are applied.

If you are required to pay a means-tested fee as a contribution towards the cost of your care, how much you are asked to pay is determined by Services Australia based on their assessment of your affordability. Essentially, they review your assessable assets and income and conduct a means-test assessment. The problem is that you start paying fees from the day you move in, but it may take 6-8 weeks (or longer) for the assessment to be done and your fee to be advised. In the interim, your care provider will be unsure how much to charge you.

This is where interim fees come in. While waiting for Services Australia to calculate and advise the fee, your care provider can set an “interim means-tested fee” and charge this amount. Each provider decides how they will set this interim fee. They might:

Charge the maximum of $400.08 per day

Set the fee at a lower amount, based on an average paid by their residents, or

Use a calculator to estimate what you might be asked to pay and charge somewhere around that amount.

Whichever option the care provider chooses, if they charge you too much, the excess does come back to you (as a refund or a credit) once Services Australia have advised the results of their assessment.

While the higher-than-expected fee might only be a temporary glitch, it can still cause considerable stress and cashflow problems in the first few months. Three practical tips to help your situation include:

Ask your care provider for their policy so you know what to expect

Fill in your means-test assessment forms as quickly as possible to minimise assessment delays by Services Australia. If you receive a payment from Centrelink or Veterans’ Affairs, check all your details are correct and up-to-date.

Make sure you have left enough money in your bank account to cover these fees.

If you are making the move into residential care (or helping a family member), we can provide independent financial advice to remove the uncertainty and help you choose the best strategy for you. Very often aged care providers will accept the fees that we calculate in our independent financial advice document and use them to set your interim fee – making it a fee that is more affordable and closer to your expected actual fee.

Phone our office on 1300 451 339 to make an appointment to discuss your situation and find out how we can help.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 25 March 2024.

Moving into residential aged care can be a stressful period with complicated rules, family conflicts and rushed timeframes. This can easily lead to mistakes, which can be costly and difficult to rectify. This article highlights three common mistakes and tips to avoid the traps

Rushing your decision

The biggest expense you will face is the cost of your room, which is likely to be quoted as hundreds of thousands of dollars. However, you might choose to pay a daily fee instead of the big lump sum.

When signing contracts, many people feel pressured to make quick decisions which might lock them into arranging a quick sale of the home. We recommend you take time to make an informed decision and understand your options. Your provider must give you 28 days after moving into care to decide how to pay. This gives you time to get advice and be prepared.

Focussing on just day 1

You need to know what fees you will be asked to pay on the first day of your stay in residential care. But this is just your starting point as your fees change over time.

Decisions you make after entry and changes to your circumstances can impact your fees. Make sure you get an understanding of what to expect over the following 2-5 years, with projections showing expected changes in fees, age pension, cash flow and asset values.

Filling-in forms incorrectly

Services Australia needs to review your financial position to calculate your fees. To enable this assessment, you need to complete some forms and update Centrelink (or Veterans’ Affairs) records.

If you don’t fill in the right form, or make mistakes with the information provided, your fees might be incorrectly calculated or cause long delays with the assessment.

Get advice

Even if your situation seems simple, there are so many aspects to consider in working out the best financial strategy. The value of seeking advice from an accredited aged care adviser is peace of mind to ensure you have made the right decisions to generate enough cashflow while protecting the value of your estate.

If you want to talk through your options or find out more information for your situation, call our office on 1300 451 339 to arrange an appointment.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 19 March 2024.

The HEAS (previously known as the Pension Loans Scheme) is a loan offered to eligible individuals by the Government and is paid by Services Australia.

The loan is secured against your family home or other eligible real estate that you nominate and may provide you with access to regular loan instalments to support your cash flow, or lump sum loan amounts.

The maximum and ongoing amounts that you may receive will be based on a number of factors, such as your age, the value of the property you use as security for the loan and the amount of any pension you may be entitled to.

Interest is payable on the loan (currently at the rate of 3.95%) and the loan plus interest must eventually be repaid.

Before you enter into the HEAS, there are a number of important things to consider. These include the long-term implications on your financial situation, the ability to fund future expenses, how a change in your circumstances could impact your debt and the impact on your estate planning arrangements. Below we summarise some of the important facts about the scheme and what you may need to think about before entering into it.

Am I eligible?

You may be eligible if you receive the Age Pension, Disability Support Pension or Carer Payment, or you would be eligible but you don’t qualify because of the income and/or assets test.

Other eligibility rules require that:

you or your partner are Age Pension age (or Department of Veterans’ Affairs service pension age), and

you are not a bankrupt or subject to an insolvency agreement, and

you have adequate real estate to offer as security for the debt, and

you have appropriate and adequate insurance covering the secured property.

The property provided as security for the loan must be Australian real property. It may be the family home, an investment property, vacant land, farmland or a commercial property. The Government will place a statutory charge or caveat on the property which means the property cannot be sold or ownership transferred unless the charge is removed (ie by paying off your debt) or is transferred to another property.

How much can I borrow?

The maximum amount that you can borrow is determined by a formula which is based on your age (or your partner’s age if they are younger than you) and the value of the real estate used as security. Once the borrowing reaches your maximum loan amount, no additional loan payments can be made. However, interest will continue to accrue until it is repaid. This means that the total debt owing in the future may exceed your maximum loan amount.

If you already have a mortgage against the property you’re using as security, or you nominate a particular value of the property to be excluded, this will further reduce the amount you’re able to borrow under the HEAS.

How can I receive the loan amounts?

You will usually receive loan instalments as regular fortnightly payments (which, if you’re eligible for a pension, will be paid with your pension each fortnight). You may also choose to receive up to two advance lump sum amounts each year subject to a limit.

Receiving fortnightly payments

The regular amount you receive will depend on several factors, including:

whether you’re entitled to a pension, and

the amount of pension you’re entitled to

Generally, the maximum amount you can receive each fortnight, including any pension you’re entitled to, is 150% of the full rate of Age Pension[1]. This means:

if you aren’t eligible for a pension payment, you can receive fortnightly HEAS loan instalments of up to 150% of the full rate of Age Pension

if you receive the full rate of pension, the maximum fortnightly loan instalment you can receive is equal to 50% of the full rate of Age Pension

if you receive a part pension, the maximum fortnightly loan you can receive is the difference between the pension you receive and 150% of the maximum rate of Age Pension

You can make changes to your fortnightly loan instalments anytime by notifying Services Australia online via your Centrelink account or completing and submitting the SA497 form to Centrelink.

Receiving lump sums

If you need access to a greater amount, you may be able to elect to receive up to two lump sum amounts in any 26 fortnightly period. The maximum combined total of the lump sums is equal to 50% of the maximum annual rate of Age Pension and this may reduce (including to zero) any fortnightly instalments for a period of time.

Are there any fees or costs?

In addition to interest costs, you will need to pay any costs involved in registering the charge (mortgage) against the property. This may be paid at the time of registration or added to your loan balance. If these costs are added to the loan balance, they will attract interest in the same way as the loan payments. You (or your estate) are also responsible for the subsequent cost of removal of the charge.

Are loan payments taxable?

The fortnightly loan instalments and any advance lump sum loan payments are not taxable; however, Age Pension payments are taxable.

Will the HEAS loan payments impact my social security entitlements or aged care fees?

The fortnightly instalments and lump sum payments are not income for the income test. However, if you don’t spend these amounts, or you use the loan to purchase or invest in an assessable asset, Centrelink needs to be updated, and this may impact your ongoing entitlement. For example, if you deposit the amounts in a financial investment such as a bank account, these amounts are not assessed for the assets test until 90 days after they are received. For the income test, the amount is deemed together with the balance of your bank account and other financial investments.

Is it possible that the debt I owe may be more than the value of my home?

A feature of the HEAS is a ‘no negative equity guarantee’ (NNEG). This means your HEAS debt will not exceed the market value of your loan at the time of repayment and you will not have to repay more than the market value of your property.

However, the NNEG may not apply if:

you put a charge or encumbrance on the secured property after taking the HEAS loan and it prevents the Commonwealth from recovering the debt

you engaged in fraud or misrepresentation regarding your participation in the HEAS

the value of the property reduces due to deliberate damage caused by yourself or a person who occupied the property with your consent, or

the sale of the property was not conducted on a fair and reasonable basis or in good faith.

When must the loan be repaid?

The HEAS loan can voluntarily be repaid partly or fully at any time. The loan plus any legal costs and accrued interest will eventually need to be repaid and, in some cases, a change of circumstances may initiate the requirement for the debt to be repaid in full. It is very important to understand the circumstances that can trigger the need to repay the loan and to understand the potential implications for your circumstances.

Change of circumstances including property sale

If you intend to make any changes to your circumstances, including plans to sell the property, you must notify Services Australia. Services Australia will arrange for the debt to be repaid when your property settles or you may provide another eligible property you own to secure the loan.

What if I pass away?

If you pass away and you have no surviving spouse or if your surviving spouse is not eligible for HEAS in their own right (for example, because they have not reached Age Pension age), Services Australia will initiate collection of the debt from your deceased estate. It is important that your surviving spouse and/or the executor or administrator of your deceased estate is aware that the HEAS debt must be repaid at this time. You and your family must consider how the debt would be repaid in this event and what will happen if the home must be sold to repay the debt, especially if you expect to have family continuing to live in the home.

If you pass away and your surviving spouse is eligible for HEAS, repayment of the loan is not required until your spouse passes away. Services Australia will initiate collection of the loan 14 weeks after your spouse’s death (Bereavement period). Your spouse may also pay the loan partly or fully at any time.

Interest will continue to accrue until the loan is fully paid.

What else should I consider and what are the risks?

Your HEAS loan will reduce the available equity in your property over time. Interest will accrue at a faster rate if no repayments are made. The HEAS loan will be collected if you sell the secured property or from your deceased estate, whichever happens first. This may mean the inheritance you leave to your beneficiaries may substantially reduce. The HEAS loan may also have unintended consequences on the distribution of your deceased estate. It is important that you seek independent legal and financial advice. You should ensure that if you do enter into the HEAS, that your estate planning arrangements are reviewed and updated if necessary. Also, you may wish to speak to your family and other beneficiaries about your intentions.

You must submit supporting documents to help Services Australia confirm the information in your application such as your age, identity, your partner’s details, bank account, tax file number and proof of your Australian residence. You may need to provide visa information and citizenship details.

You will need to provide details relating to the secured property such as loan agreements, contracts and the most recent mortgage statements and other documentation. If you are a couple, both you and your partner must sign the application form. If you are separated from your partner, you must provide separation details.

Appendix: Example calculation of maximum HEAS amount and payments

The maximum loan amount is determined based on age, as well as the value of the real property you use as security. Your age (or your spouse’s age if they are younger) is used to determine the ‘age component amount’. This amount is a dollar figure and is set out by the Department. Speak to an independent financial adviser to find out more.

The maximum amount you can borrow is calculated as:

Age component amount x Value of real assets/$10,000

Where:

Age component amount is a dollar figure which is based on your age last birthday. For members of a couple, the age component amount is based on the age of the younger spouse.

Value of real assets is generally the value of the property provided as security, less your nominated amount and reduced by any other charges over the asset(s). The value of real assets will be rounded down to the nearest $10,000.[2]

For example, if you turned 70 on your last birthday, your age based amount is currently $3,080. If you offer your family home as security and it’s worth $1,000,000 with no debt currently secured against it, your maximum loan amount will be:

$3,080 x ($1,000,000/$10,000) = $308,000.

Your maximum loan amount will be recalculated in another 12 months after your next birthday.

The maximum fortnightly amount of loan instalments you’d be eligible for (as at 20 March 2024[3]) would be:

$558 per fortnight if you’re a single homeowner and you receive the full age pension (ie 150% x maximum Age Pension rate of $1,116, less your Age Pension payment of $1,116)

$1,674 per fortnight if you’re a single self-funded retiree who is a homeowner (ie 150% x maximum Age Pension rate of $1,116 less $0, as you’d not receive any Age Pension)

An amount between $558.15 and $1,674.45[4] per fortnight if you’re a single person entitled to a part Age Pension.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Effective from 20 March 2024

[1] Includes the basic rate of Age Pension, the pension supplement, Energy Supplement and Rent Assistance if applicable.

[2] If value of assets is less than $10,000, the value is nil.

[3] These amounts will change in line with changes to the Age Pension rate, which may occur on 20 March and 20 September each year.

[4] The maximum possible loan instalment $1,674.45 per fortnight, less the minimum pension supplement $43.90 and the energy supplement $14.10.

Second marriages may present additional financial challenges when balancing day-to-day expenses with implications for aged care funding. You may not share finances equally, but Centrelink/DVA will assess your obligations as if you do.

Life is full of ups and downs. You might have been unlucky and lost a spouse, but then been lucky to find love again. A new relationship can bring companionship and support but may also bring financial challenges, especially with funding aged care and estate plans.

Some couples may be willing to share a life but may prefer to keep finances separate so inheritances can pass to their own children and family. If you and your partner enter the relationship with differing levels of savings and assets, as a couple you will need to decide how to split or share resources. You may also need to decide whose home to live in or whether to buy a new home.

These decisions need to balance your life plans and your estate plans. You may wish to consider how to ensure your partner is looked after if something happens to you, while also protecting the estate for your own children. These might be conflicting objectives.

From a Centrelink and aged care view, two people living together in a relationship are assessed as a couple. Assets and income are combined and then split equally – regardless of who owns what or how you want to divide your finances.

What defines a couple

If you receive a Centrelink/Veterans’ Affairs (DVA) benefit and your relationship status changes, you need to notify Centrelink/DVA and update your records.

Whether two people are considered to be a couple depends on five aspects, including:

Financial aspects

Nature of the household and how household chores are shared

Social aspects and how the two people present to family and friends

Any sexual relationship

Commitment to a permanent and ongoing relationship on an intimate level.

No single factor is definitive in determining status as a couple. An assessor may look at the facts of the case and interview the people involved as well as friends and family to determine whether the two people live separate or shared lives.

The impact on aged care

If your or your spouse need to access aged care services, assessment of your financial capacity (and contribution towards the costs) will use the same relationship status rules that apply for Centrelink/DVA.

If you are a couple, fees are based on half of the combined assets and income. This may see a person moving into care needing to pay fees greater than their individual affordability and needing the other spouse to help with the costs. How this help is provided should be decided with independent financial advice to fully understand the implications. For example, if the person staying at home uses some of their assets to pay accommodation costs as a lump sum for a spouse moving into residential care, this money will eventually be returned to the estate of the care recipient. This means the money may find its way into the other family’s hands, rather than back to the spouse who made the payment.

We can provide advice to help you navigate the rules and consider strategies that are as fair as possible to both members of the couple. This may help to minimise family conflicts. Call us on 1300 451 339 to make an appointment.

Samantha Chivers, Client Services Administrator and Aged Care Consultant

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 4 March 2024.

The recently released Intergenerational Report highlights trends and impacts over the next 40 years and highlights the significant impact of an ageing population. A major theme in the recent Intergenerational Report was the impact on Australia’s economy and society of an ageing population, which will lead to a rising demand for aged care over the next 40 years. This reinforces the importance of considering aged care needs ahead of a crisis situation. The care and support sector was singled out as one of the key sectors expected to grow over the next four decades as it expands to accommodate the needs of an increasing number of older Australians. In particular, the 85 plus age group is expected to triple over the next 40 years.

Meeting demand will require ongoing investment and improvements in the delivery of aged care services. But with predictions of budget deficits for the next 40 years, the ability for the Government to fully fund the increasing cost pressures is limited. A greater and increasing share of costs will likely need to be met by the person accessing care services, where they have the financial means to do so. Australians need to plan ahead for their aged care needs. Aged care considerations should form a key component of retirement planning to take into account the costs and related financial decisions.

While longer life expectancies will see Australians spending more years in full health, on the flip side, we are also likely to experience an increased number of years in ill-health. This will in turn accelerate spending in health and aged care as well as demand for services and advice. As shown in the chart below, the average number of years that a person lives in ill-health has been steadily increasing across the last decades and this trend is expected to continue to grow.

Source: Australian Institute of Health & Welfare, Australian Burden of Disease study, 2022.

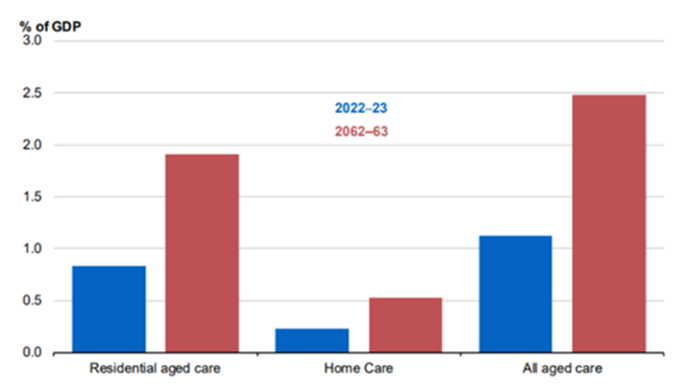

Most Australians who reach old age will need aged care services. The Australian Government provides the majority of funding, across both residential aged care and home care services, with users contributing a small portion of the costs. Government spending on aged care is projected to grow from 1.1% of GDP to 2.5% in 2062-63 and aged care spending per person will also increase. The composition of government spending across the home care and residential care is shown in the graph below.

Source: Treasury

Without a doubt, Australians need to consider aged care options and strategies not only for their own future needs, but also the needs of older parents or other family members. If you would like to start the discussion and explore your options, contact us today on 1300 451 339 to arrange an appointment.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 15 December 2023.

When your family gathers over the festive season, it might present an opportunity to start planning for future care needs.

Christmas is a time for families and the New Year is for resolutions. This year, combine the two by making a resolution to pay more attention to how your older parents are coping and start family conversations to develop a plan for future care and support.

You may have been busy through the year and not noticed the small things. But how well parents are coping may become more obvious when you have time to catch up with family over the festive season.

You might not want to face that your parents are getting older and may need help. If you are the older person, asking for help does not have to be the start of a slippery slope. Rather, it might be the first step to having greater control over your future independence and reduce some of the daily strain on yourself and other family members.

It might be time for a family meeting

Planning is the key. And planning early gives the best outcomes.

Retirement plans should consider how to manage the frailty risk that might be experienced in the later stages of retirement. Bringing family into the conversation may help to minimise conflicts within your family and help everyone be comfortable with decisions that need to be made.

Families getting together at Christmas, might offer one of the rare opportunities within a busy year to hold a family meeting. For the older parent, this offers the chance to make yourself heard and express your wishes. For the children, it can help to remove uncertainty and share the responsibilities. These discussions are more effective if they are started early, while parents are still able to maintain control and independence.

A well-run family meeting can allow parents, children and other important family members to discuss issues and preferences, express concerns and make decisions that work for the family as a whole.

If thought of this discussion fills you with dread, we can offer support and independent financial advice. We inject a neutral voice and experience into what can be an emotional discussion.

Tips for starting a conversation

Some tips for families to consider over the festive season include:

Be observant for signs that parents may not be coping

Compare observations with other family members

Talk to your parents about their future plans, concerns and living arrangement options

Start researching aged care options (including home care) and understand the costs

Check that enduring power of attorney documents and wills are in place and still relevant – seek legal advice to review and update documents

And, if care is needed now, contact myagedcare.gov.au to arrange an assessment.

Make an appointment to discuss options and actions needed to be taken. Call us on 1300 451 339.

IMPORTANT INFORMATION: This document has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice.

No-one wants to be living with dementia. Keeping an active brain may reduce your risks and promote good cognitive health for longer.

With an increasing number of people living with dementia in Australia and around the world, research activities aim to understand how the brain works and look for ways to reduce or slow the risk of dementia. Across the globe,10 million new cases of dementia are diagnosed each year.